Credit cards and phone. Image: 279photo Studio/Shutterstock

As more and more banks shut their branches, we looked at what it’s actually like to go mobile-only in the banking world.

Those who have remained reliant on the services that bricks-and-mortar banks provide could soon find themselves left behind in an increasingly mobile world.

A quick look back at some of the stories from this year confirms that banks are trying to move away from having staff answering queries at desks, instead favouring banking online, over the phone, or even through intelligent chatbots.

Last month, Ulster Bank announced that it was to close 22 branches across Ireland, saying that as few as 30 people were using each of them every day.

Similarly, AIB announced in February that it was to close half of its 30 branches in Northern Ireland, once again citing “the considerable shift in customer behaviour and their changing needs”.

Due to the onset of a fintech revolution, some banks who don’t follow the traditional model are going one step further, bypassing physical locations and being entirely based within a person’s smartphone.

To name just a few in Europe, Atom, Starling Bank and Hello Bank are now all offering current accounts without a single branch, aside from their own development offices.

To put some of them to the test, we looked at two neo-banks that are growing rapidly: N26 and Revolut.

Diving head first into this new world of banking, I decided to go with German-based N26.

The fintech start-up has shown substantial growth in recent years, particularly in Ireland, where it already claims 10,000 account holders and recently opened self-employed accounts here.

So, what is it like to set up?

First you have to decide what type of current account you want. Depending on your needs and finances, it could cost more than you expect.

In N26’s case, you can either sign up for a free account – as I did – or you can pay €5.90 per month for a premium one.

That €70 will guarantee you insurance, for everything from ATM theft to holiday insurance, as well as free ATM withdrawals in foreign currency.

During the sign-up process, you deal with a representative at one of N26’s offices who takes you through the steps of showing your passport and providing some other information as well as your headshot.

(Be warned: make sure you sign up somewhere with adequate internet as my connection cut out two times, resulting in me being in the middle of signing up, only to be cut off and subsequently having to deal with three different representatives.)

All in all, the process only lasted a few minutes and I was promised that my card would be sent out within a week, which it was.

A Revolut user spoke to me about their own experience signing up with the British-based start-up and described it as being similarly easy.

The only difference is that with Revolut, there is a €6 sign-up fee paid through the app.

What is it actually like to use?

Once I had activated my card in an ATM and connected it with the app, it was good to go.

With N26’s free account, you get most of the services that you get with the premium one, but there is a limit of five free ATM withdrawals over the course of a month.

After that, it is €2 per withdrawal, which shows the company’s focus on getting its users to ditch cash in favour of contactless and digital payments.

Unfortunately for Apple Pay or Android Pay users, both N26 and Revolut are incompatible, so you will still have to use your card for these payments.

Overall, buying groceries or any other goods using contactless payment is fantastic.

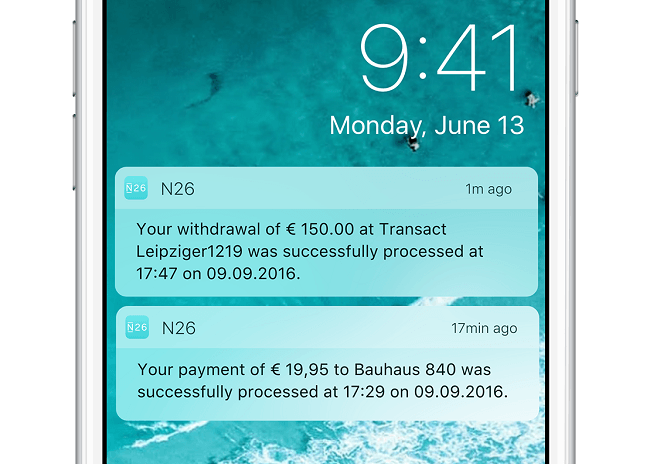

Within seconds of making a payment, a notification appears on your phone telling you what you spent and where you spent it, all logged in the app.

A screenshot of notifications after a payment has occurred. Image: N26

What does the app do?

The app is the nerve centre of your bank account where you will manage all your funds, from arranging a payment to someone, to checking your spending habits.

It allows you to look at what you’ve spent over the past few months and customise some tags so you can organise your spending a bit better.

Perhaps the best features are the ability to simply press a button and turn your card off in the event your wallet gets stolen or lost, as well as being able to control spending money abroad.

These features are not limited to N26 or Revolut, however.

Is it geared towards people who travel a lot?

Based on my own reason for signing up to it – and those who I have spoken to for this piece – a prepaid debit card is ideal for those regularly on the move.

Looking at Revolut, the start-up has appealed to a lot of travellers as the exchange rate on purchases and transfers are made at the value of the currency at that very moment of order, unlike many traditional banks.

As one Revolut customer puts it, having a prepaid card in addition to their traditional bank account offers “peace of mind”.

By topping up this card on your travels, the risk of losing everything is diminished – a similar reason I signed up to N26.

This is also why the Revolut user said he would recommend it to his globetrotting friends, and I would too.

Line of people queueing up to withdraw money at ATMs on street of Old Havana area. Image: TRAN THI HAI YEN/Shutterstock

Are there any negatives?

Strangely, one of the downsides of these latest mobile banking companies is also one of its advantages: instant payments.

While it makes business sense to encourage users to invite more friends to use the service, in order to gain access to instant payments for things such as bill-sharing, the process for those who aren’t customers is a lot more complicated.

For both N26 and Revolut, account holders of other banks need to enter their details every time in order to receive a payment, which is just time-consuming and not exactly ideal.

This is not necessarily a problem with one company, though, as the seemingly unfixable problem of bank cooperation is unlikely to see instant transactions across the board anytime soon.

Final thoughts?

In Ireland, there is nothing stopping you from using one of these banks as your main current account. You could get your pay cheque sent via one of these platforms as they all comply with EU regulation and, more importantly, your money is protected under EU law.

However, from my own experience and from talking to others, the general consensus appears to suggest that these mobile banks are mostly being used for options abroad.

Just like the opening up of the banking sector to new start-ups encourages cheaper fees with greater competition, the ability to travel for less is also a very welcome addition.

There is no doubt that these new banks, whichever one you may choose, offer some real benefits for those looking for an alternative to traditional banking. It’s just a matter of finding the one to suit your needs.